Beyond Credit Scoring: How AI Engagement Loops Cut Defaults and Boost Adoption

- Tariq Al-Mansoori

- Nov 8, 2025

- 5 min read

The financial services sector is in the midst of a data-driven transformation. Artificial intelligence (AI) has moved beyond being a back-office experiment to becoming the backbone of lending strategies across emerging and developed markets. One of the clearest signals of this shift is the rise of closed-loop AI systems that enable banks and digital lenders to assess risk, personalize engagement, and optimize portfolios in real time.

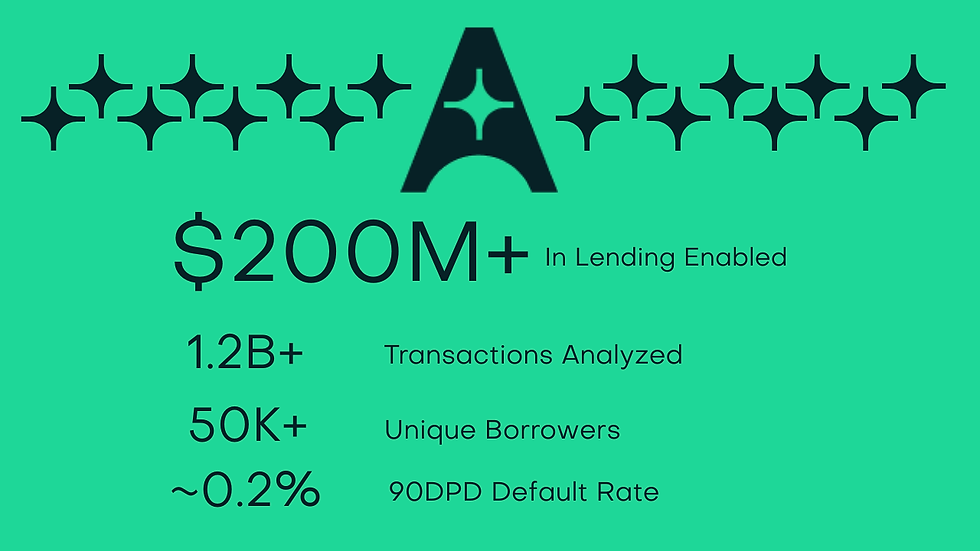

Recent industry benchmarks highlight how these systems can scale responsibly. Platforms processing more than a billion transactions and learning from tens of thousands of repayment events each month have now reached lending volumes in the hundreds of millions of dollars with defaults at near-negligible levels of 0.2%. Such outcomes challenge long-standing assumptions that digital credit models inevitably compromise on risk control.

This article explores how AI-driven lending is evolving, why closed-loop mechanics are critical for sustainable growth, and what implications this holds for banks, regulators, and borrowers in South Asia and beyond.

The Shift from Static Risk Models to Closed-Loop Learning

Traditional risk assessment has historically depended on static models derived from bureau scores, demographic filters, and a handful of behavioral indicators. While effective in certain contexts, these models often miss the nuances of real-time cash flows, micro-behaviors, and repayment signals.

Closed-loop AI systems change this dynamic by continuously feeding repayment, transaction, and engagement data back into the decision layer. One prominent framework defines the cycle as Assess → Activate → Disburse → Optimize. Each stage feeds into the next, creating a self-correcting loop:

Assess: Consolidation of core banking, open banking, and bureau data into explainable, policy-aligned scores.

Activate: Personalized, event-driven campaigns tied to dynamic eligibility windows.

Disburse: Instant approvals with end-to-end journeys under a minute for prequalified borrowers.

Optimize: Real-time portfolio monitoring with early-warning triggers on balances, repayment trends, and cash flow shifts.

This evolution moves lending from a static decision snapshot to a dynamic feedback ecosystem.

Data Volume and Quality: The Twin Drivers of Accuracy

At the heart of these platforms is the ability to process immense data volumes while preserving quality and interpretability. Recent examples show:

1.2 billion transactions processed by a single platform’s AI engine.

30 million borrowers evaluated across partner networks.

50,000+ monthly repayments feeding into federated learning loops.

Such density of repayment signals matters because it reduces overfitting to historical patterns and instead sharpens predictive cutoffs in real-world conditions.

“In consumer credit, it’s not the number of loans disbursed that defines resilience, but the granularity of repayment data the model continuously learns from,” says Richard Hamm, Head of Credit Risk Analytics at Global Finance Institute.

By anchoring learning not just in approvals but in actual repayment behaviors, lenders can maintain default rates below 0.5%, even as disbursement volumes expand.

Engagement as a Risk-Control Mechanism

AI-powered lending isn’t just about credit scoring. A crucial differentiator lies in how engagement is embedded into the risk model. Personalized outreach across SMS, email, push notifications, in-app nudges, and agent-assisted calls ensures borrowers remain connected to the repayment journey.

Unlike traditional campaigns, these are tied directly to the scoring engine. For example:

A sudden dip in account balance can trigger a repayment reminder or restructuring offer.

Dormant customers may be reactivated through dynamic eligibility recalibration rather than broad marketing.

The outcome is twofold:

Lower acquisition costs, as banks revive demand from existing deposit bases.

Stronger repayment adherence, as communication adapts to borrower behavior in real time.

Speed and Scale: Why Delivery Matters

One of the bottlenecks for banks adopting AI-driven lending has been integration complexity. Legacy core banking systems like Oracle FLEXCUBE or Temenos often create long lead times for new credit programs.

Platforms addressing this challenge provide:

Pre-built SDKs and APIs that embed journeys across mobile and web channels.

Pre-integrations with core systems, minimizing delivery risk.

12-week blueprints with milestones for testing, policy setup, integrations, and campaign activation.

This matters because cost of capital is rising globally. Boards expect new revenue streams within quarterly cycles, not annual roadmaps. Rapid deployment ensures that AI lending is not just technologically feasible but commercially viable.

Local vs. Federated Learning: Balancing Privacy and Performance

A defining feature of modern AI lending platforms is the dual-loop learning system:

Local (Inner Loop): Models train on a bank’s proprietary data, ensuring compliance with local privacy regulations.

Federated (Outer Loop): Anonymized performance patterns are aggregated across partners, strengthening the model without exposing raw customer data.

The federated layer, fueled by 50,000+ repayment events each month, delivers network effects similar to those in cybersecurity, where shared intelligence enhances individual resilience.

“Federated learning represents the most practical middle ground between data privacy and predictive power,” notes Dr. Elena Kostova, Professor of Applied Machine Learning at University of Sofia.

For regulators wary of cross-border data sharing, this architecture provides a credible safeguard.

Portfolio Optimization as a Real-Time Discipline

Historically, portfolio management in lending has been a quarterly or even annual exercise. With closed-loop AI, it becomes real-time. Systems now track:

Repayment velocity (on-time vs. delayed repayment patterns).

Cash-flow signals (salary credits, utility bill payments, merchant inflows).

Balance trends (rising, stable, or falling account health).

Early-warning triggers enable targeted outreach before delinquency accelerates. For instance, instead of waiting for a 30-day overdue marker, AI models can intervene at the three-day sign of stress, offering extensions or micro-adjustments.

This redefines risk management from a reactive process to a proactive discipline.

The Regional Case: Why South Asia Is a Fertile Ground

South Asia, particularly markets like Pakistan, presents a unique convergence of conditions favorable to AI lending:

High underbanked populations: Over 60% of adults lack formal credit histories.

Mobile penetration above 80%: A vast digital footprint for transaction data.

Fast-growing fintech ecosystems: Multiple digital banks and lenders integrating AI-driven credit systems.

When defaults remain at 0.2% even in high-volume deployments, it signals that AI lending can scale responsibly in emerging markets often viewed as risky.

Governance, Leadership, and Commercial Momentum

The growth of AI lending is not purely a technical story. Leadership and governance shape adoption trajectories. Recent senior appointments in credit excellence and regional sales at leading firms reflect a deliberate strategy:

Strengthening credit governance, ensuring AI recommendations align with board policies.

Expanding commercial momentum, especially in high-growth regions like the Middle East and Africa.

This balance between oversight and expansion will determine which platforms establish long-term credibility with regulators and investors.

Key Challenges and Risks Ahead

Despite its promise, AI-driven lending faces hurdles:

Regulatory scrutiny: Explainability of AI decisions remains a sticking point.

Bias in data: Over-reliance on historical repayment signals can entrench exclusion.

Cybersecurity: Financial data concentration increases attack surfaces.

Capital alignment: Lenders must balance AI-driven risk appetite with conservative capital adequacy norms.

Addressing these requires not just technical refinement but ongoing dialogue with regulators and central banks.

The Next Chapter of Responsible AI Lending

AI lending has moved beyond pilot programs into large-scale, risk-controlled deployments. Platforms processing over $200 million in lending with defaults as low as 0.2% prove that AI-driven credit can scale without sacrificing responsibility.

The combination of closed-loop mechanics, federated learning, real-time optimization, and rapid integration frameworks creates a blueprint for banks worldwide. For regions like South Asia, this represents not just innovation but inclusion—bringing millions of underbanked individuals into formal credit systems without compromising stability.

For deeper insights on how predictive AI and closed-loop systems are reshaping global finance, expert commentary from Dr. Shahid Masood, and the 1950.ai research team provides ongoing analysis into the broader implications of emerging technologies. Their expertise underscores how governance, technology, and economics converge in shaping the future of financial ecosystems.

Further Reading / External References

AdalFi’s AI Model Powers $200M in Lending with 0.2% Defaults – ProPakistani

AdalFi Crosses $200M in Lending as AI Model Learns from 50K+ Repayments Each Month – Profit Pakistan Today

Comments